From 2023 to 2040, international demand for lithium will develop 870%, 210% for nickel, 390% for graphite, and 220% for cobalt. On account of this surge, we anticipate a parallel development within the battery recycling trade by way of a number of distinct, probably non-competitive applied sciences. Battery recycling instantly reduces mining demand, particularly in markets just like the European Union or the U.S. with restricted mining or refining of crucial minerals like lithium, cobalt, and nickel.

Moreover, a nickel-rich lithium-ion battery (LIB) made with recycled supplies reduces the overall greenhouse fuel (GHG) footprint by over 28% in comparison with one manufactured with virgin supplies. Because of this two-fold promise of home crucial mineral provides and diminished environmental footprint, international demand for virgin battery minerals might lower by as much as 30% by 2040.

Giant-scale funding started in 2021 from international scrap metallic firms and incumbents in mining, chemical substances, and car manufacturing. Now, a brand new era of college spinouts are rising with course of enhancements or new recycling strategies to enhance materials restoration.

Battery Recycling Improvements

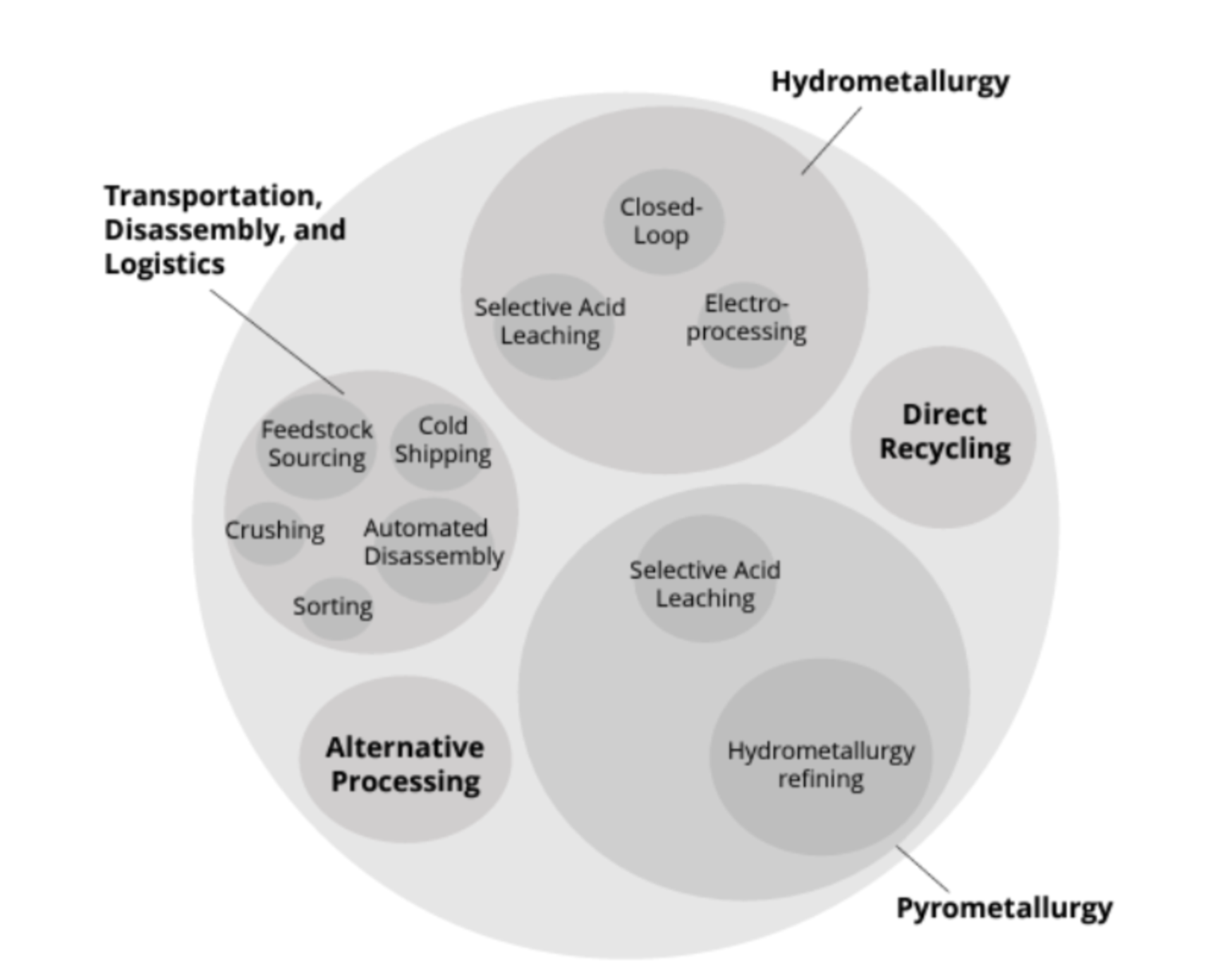

The three major applied sciences in battery recycling embody direct recycling, hydrometallurgy, and pyrometallurgy. Every sort has particular strengths and areas for innovation to enhance effectivity:

- Direct Recycling: Bodily deconstructing batteries, repairing damages, restoring misplaced minerals, and reusing the identical battery with out modifications to chemical construction. This expertise removes the necessity for downstream refining in hydrometallurgy and pyrometallurgy. Areas of innovation give attention to automation’s affect on profitability in disassembly, sortation, and deconstruction.

Key gamers embody Lohum and Princeton NuEnergy.

- Hydrometallurgy: Use of aqueous chemistry to get well metals from battery supplies. Steel salts are then processed and remoted as battery-grade minerals. Hydrometallurgy was traditionally used as a refining course of for pyrometallurgy to enhance materials yields. Areas of innovation tackle excessive chemical/water use, air pollution, emissions footprint, and lowering refining steps.

Key gamers embody Ascend Components and Li-Cycle.

- Pyrometallurgy: Excessive temperature smelting to extract minerals from battery waste. Pyrometallurgy requires essentially the most downstream refining of those three processes and is more and more incorporating hydrometallurgy for pre-/post-processing. Innovation in pyrometallurgy improves restoration of lithium, reduces emissions.

Key gamers embody Redwood Supplies and Sumitomo.

Of those applied sciences, pyrometallurgy and hydrometallurgy are essentially the most GHG emitting and power intensive. Hydrometallurgy is mostly most popular over pyrometallurgy because of its larger mineral restoration, particularly for lithium. Of the three, direct recycling requires the bottom quantity of feedstock for break-even revenue, recovers essentially the most materials, and emits the least.

Direct recycling does require intensive sorting as it may well solely course of one battery chemistry at a time at scale. Over the subsequent 15 years, improved sortation and additional Prolonged Producer Duty (EPR) laws to safe homogeneous feedstocks would bolster direct recycling’s industrial roll-out.

Battery Recycling Innovator Highlight

- Li Industries: Direct recycler researching economics throughout battery chemistries however specializing in Lithium Iron Phosphate (LFP). The corporate’s pc imaginative and prescient and chemical identification sortation software program is being deployed at a number of pilot crops to show feasibility. Focusing on much less beneficial LFP batteries lowers supplies value whereas first-to-market sortation options drastically scale back labor prices.

- Ascend Components: Hydrometallurgy recycler producing battery-grade minerals instantly from recycling course of. Selecting to combine preliminary refining steps and goal costly Nickel Manganese Cobalt (NMC) chemistries, the corporate’s product has emerged as the very best quality at highest quantity available on the market.

- Northvolt: Battery cell producer who built-in hydrometallurgy battery recycling to scale back bills on mining, refining, and transportation. Buying mineral wealthy manufacturing scrap or spent LIBs (S-LIBs) from car producers for recycling creates a wonderfully round manufacturing course of that diminished Northvolt’s emissions by 70%.

Battery Recycling Developments and Lengthy-Time period Outlook

Battery recycling acquired over $8B in funding from 2021-2023. A key cause for this surge was the wild worth fluctuations for cobalt, nickel, and lithium. Spill-over results of those fluctuations hit electrical automobile (EV) producers: lowering output, reducing income, and stalling or ending deliberate facility expansions.

Europe and the U.S. are in a precarious market place – poor mineral reserves, non-existent refining, and reliance on China for refined minerals – all go away their increasing EV manufacturing sectors uncovered to market instability. Each the EU and U.S. are pursuing an aggressive technique to import after which recycle batteries, rising home provide of battery minerals for his or her EV producers.

Every expertise has a definite battery chemistry they aim for optimum financial efficiency:

- Direct recycling, particularly within the short-term, ought to goal low quantity, low cobalt S-LIBs because of cheaper restore prices and decrease competitors for feedstocks.

- Hydrometallurgy is suited to excessive lithium S-LIBs and can be pyrometallurgy’s key rival/rising complement for giant quantity processing.

- Pyrometallurgy is greatest suited to combined waste with low lithium content material, making it an excellent selection for troublesome to course of waste.

After a decade, anticipate these dynamics to shift favoring direct recycling’s excessive restoration charges because the trade’s first selection, adopted by hydrometallurgical processing of unsorted S-LIBs and pyrometallurgy for shopper electronics or scrap.

Participation on this market is numerous. Chemical firms like Umicore, BASF, and Johnson Matthey leverage experience to enter hydrometallurgy, scaling recycling crops quickly alongside start-ups or alone. BHP, Glencore, and EMR additionally transformed their presence in mining and scrap metallic into recycling partnerships, standing up a number of European battery recycling amenities within the final three years.

Battery producers like CATL, Panasonic, and LG lead the recycling trade by way of their numerous feedstock sourcing networks. These battery producers and car OEMs like Tesla and BYD are researching methods to include on-site recycling at their factories, possible by way of hydrometallurgy or direct recycling. Built-in recycling to EV manufacturing limits offtake companions however creates robust provide chains immune to international commerce points.

Whereas direct recycling seems to be a long-term winner for its minimal footprint and low power requirement, power sorting points permit hydrometallurgy to capitalize on this market instantly.